A credit card’s interest rate is one of the most important features, particularly for cardholders who carry a balance on their credit cards. Having a low interest rate means minimizes the cost of paying off a credit card balance over time. But, don’t take your interest rate for granted. If you’re not careful to make your payments on time each month, you could trigger your credit card’s penalty rate.

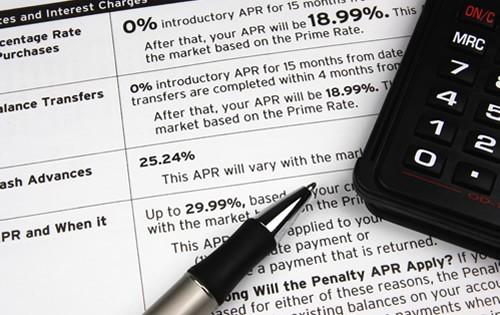

What is the Penalty Rate?

The penalty rate on a credit card is the highest interest rate charged on a credit card. As long as you abide by the terms of your credit card agreement and make your monthly payments on time, you’re safe from the penalty rate. However, if you allow your account to become 60 days past due, your credit card issuer can impose the penalty rate.

Drawbacks of Having the Penalty Rate

Depending on your credit card terms, the penalty rate could be 30% or higher. In some cases, that might be more than double your regular rate. The higher rate would significantly increase the finance charges you pay on balances you carry.=

If the possibility of paying the penalty rate on one credit card isn’t bad enough, your credit card issuer could rate the rate on any other credit card you have with the same company. The rates on your credit cards from other issuers are safe – as long as you make your monthly payments on time.

While your credit card issuer has to lower your rate for existing balances, it can keep the penalty rate in effect for any charges you made to your credit card after the penalty rate. That means you could be stuck with the penalty rate forever.

What Are Your Options?

Here’s what you should do if the penalty rate is imposed on your credit card.

Catch up on your payment as soon as possible to keep your account from becoming even more delinquent. However, your interest rate won’t go back to normal once you catch up on your payment. Instead, it will take six consecutive, on-time payments to get your old rate back.

Watch your credit card statement to see if your interest rate goes down. If not, call your credit card issuer to ask them to lower your rate. If you can’t get the credit card issuer to lower your interest rate, for future charges, you can avoid higher finance charges by paying your balance in full each month.

Transfer your balance to a credit card with a lower interest rate. Even if you can’t qualify for a promotional balance transfer rate, you can save money by moving your balance to a credit card that hasn’t received the penalty rate.

Pay off the balance and close the credit card. If you can’t get back into your credit card issuer’s good graces and get your rate lowered, considering closing the credit card completely.

I would also add: Call the credit card company and explain them your situation. Sometimes they can work with you and offer you an alternative.